Wealth tax for non-residents in Spain: what you need to know

In this article

Do you have assets in Spain but do not live there permanently? Then it is important to know how Spanish wealth tax works for non-residents. In this blog, we explain clearly when you have to pay tax, what exactly is taxed and what exemptions there are.

What exactly is wealth tax (impuesto de patrimonio)?

Wealth tax is an annual tax levied on the net wealth of natural persons. This means all your assets and rights with economic value, minus your debts and liabilities.

Residents versus non-residents: what is the difference?

In Spain, there are two ways in which people can be subject to wealth tax:

Residents are subject to the tax by personal obligation. This means that they pay tax on their entire worldwide assets, i.e. both those in Spain and abroad.

Non-residents are subject to the tax by real obligation. They only pay tax on assets located in Spain, which can be exercised there or to which obligations in Spain are attached.

What is included in the taxable assets of non-residents?

For non-residents, only assets in Spain are taxed. These include:

Real estate in Spain

Bank accounts with Spanish banks

Spanish shares and investments

Rights or obligations that can be exercised or fulfilled in Spain

When determining net assets, only debts and expenses directly related to these Spanish assets may be deducted. For example, a mortgage on a property in Spain is deductible, but a personal loan abroad is not.

Capital gains tax rates (national rate)

Spain applies a progressive rate ranging from 0.2% (for assets above the exemption) to 3.5% (for assets worth tens of millions).

Example (2024):

Regional differences

The autonomous regions (such as Andalusia, Catalonia and the Balearic Islands) are allowed to apply different rules:

Some regions (such as Madrid) do not levy any wealth tax, not even for non-residents.

In other regions (such as Catalonia or the Balearic Islands), higher rates or a lower exemption apply.

Exemption: when do you not have to pay anything?

Good news for smaller estates: there is a minimum exemption of €700,000 for non-residents. So if your net assets in Spain are below that amount, you do not have to pay wealth tax.

Please note: this exemption applies per person. In the case of joint ownership (e.g. between partners), the assets are divided proportionally.

When is the tax calculated?

Wealth tax is determined on the basis of the situation on 31 December of each calendar year. No tax is therefore levied on a period, but on the assets on that specific date.

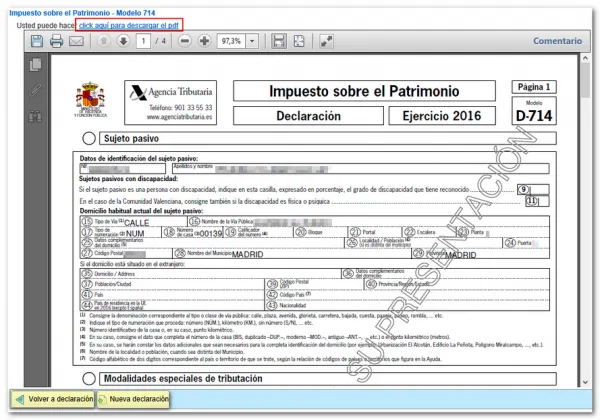

As a non-resident, you must file a tax return if your Spanish assets exceed the exemption, usually before 30 June of the following year (just like income tax). The return is filed using Modelo 714.

A special note: if, for example, someone dies on 30 December, no wealth tax is payable for that year, because the person was no longer alive on 31 December.

Conclusie

As a non-resident in Spain, you only have to pay wealth tax on assets that are actually located in Spain. Thanks to the €700,000 exemption, you often do not have to pay tax on average assets, but it is important to have this assessed annually, especially if you have multiple Spanish assets.

Do you have questions about your personal situation? Consult a tax specialist who has experience with international asset structures and Spanish legislation.

Sources and more information:Agencia Tributaria España

Tags

Related Posts

Finance & Taxes

Finance & TaxesIBI & Basura in Spain: the reference date determines who pays

When buying or selling a property in Spain, questions often arise about municipal taxes, particularly the IBI (Impuesto sobre Bienes Inmuebles, property tax) and the basura (waste collection tax). Who is actually responsible for paying these taxes when a property changes hands?

Finance & Taxes

Finance & TaxesCl@ve and the digital certificate: what are they and what is the difference between them?

Anyone who lives, works, invests or owns property in Spain increasingly has to deal with digital government services. Taxes, social security and many administrative procedures are now handled almost entirely online. In all these cases, you need some form of digital identification or electronic signature.

Finance & Taxes

Finance & TaxesEverything You Need to Know About the Change in Spanish Transfer Tax Starting Jan '22

Until the end of 2021, the purchase of existing property in Spain was subject to 10% registration (notarial transfer tax) or ITP. As of 1 January 2022, there will be a change in the calculation of transfer taxes. The cadastral reference values will now also be taken into account. We have summarised the new rules for you below: